What first-time Canadian homebuyers are leaving on the table and how their parents can help them find it.

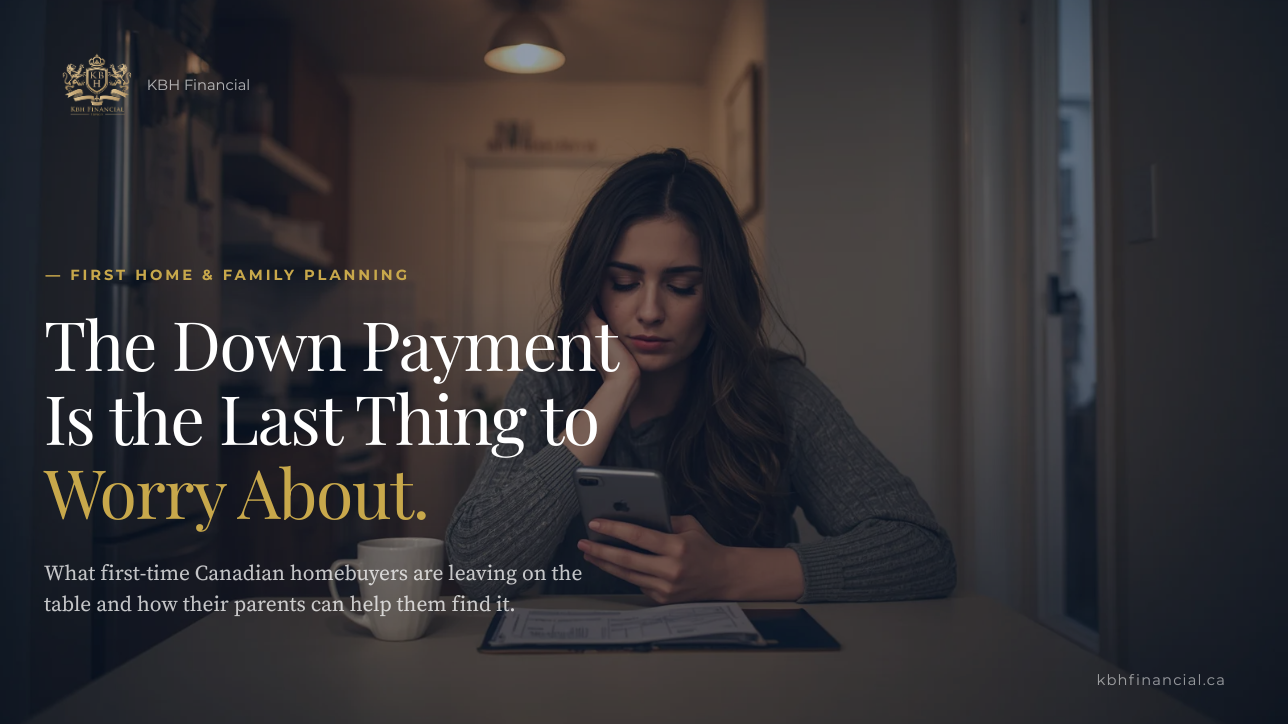

Maya did the math again on Tuesday night.

She does it the same way every time. Phone in hand, sitting at the kitchen table in the apartment she shares with two roommates in a neighbourhood she could not afford to buy in even if she had the down payment, which she does not, quite. She knows the number she needs. She knows the number she has. The gap between them has been the same number for eight months, which means it is not really a gap anymore. It is a wall.

She is 29. She has a good job. She saves what she can. And every time she runs the numbers, she arrives at the same conclusion. That the home her parents bought at her age, in this city, for a fraction of what it costs today, might simply be out of reach. Not forever. But for longer than she wants to admit.

Her parents know. They have been watching this from a distance, the way parents do. Her mother mentioned, quietly, at Easter, that they could help with the down payment. Her father nodded in the way that meant the conversation had already happened privately between them. Maya said she would think about it.

What none of them know, not Maya, not her parents, is that the government has already set aside a meaningful amount of help. It has been sitting there, waiting, in three accounts that most Canadian families either do not know about, do not fully understand, or are not using in the right order.

Before anyone transfers a dollar, it is worth knowing what those accounts are.

The Real Problem Isn’t the Down Payment

Way back in 1998, I was in my late twenties, and I bought my first home. It was a three-bedroom townhome and I paid $74,000. It was in no way luxurious, but it was only a few years old, it was very clean and all my neighbours were around my age. I had saved the previous three years to put together the $5,000 for the downpayment.

Today is a very different story…

The national average home price in Canada sits at just under $700,000 as of early 2026. A minimum five percent down payment on that is roughly $35,000. Twenty percent, the threshold that eliminates the need for mortgage insurance, is closer to $140,000. Those are real numbers and they are not small.

But here is what most first-time buyers do not know. The federal government has built three registered accounts specifically designed to help Canadians accumulate that money faster, with significant tax advantages attached to each one. Most first-time buyers are either not using all three, not maximising them, or not using them in the right order. Any one of those mistakes costs real money. All three together can mean the difference between a down payment that takes a decade and one that takes five years.

The median age of a first-time buyer in Ontario has climbed to 40, up from 36 just a decade ago. That number is not a coincidence. It is, in part, the cost of not having a plan.

Tool One: The FHSA — The Best Account Most Canadians Have Never Heard Of

The First Home Savings Account launched in 2023 and it is, without exaggeration, one of the most generous savings tools the federal government has ever created. Financial author David Chilton, the Wealthy Barber himself, called it “the greatest deal in the history of Canadian savings.” He is not wrong.

Here is how it works. You contribute up to $8,000 per year, to a lifetime maximum of $40,000. The contribution is tax deductible, like an RRSP, which means it reduces your taxable income in the year you contribute. The money grows tax free inside the account. And when you withdraw it to buy your first home, you pay no tax at all. It is deductible going in and tax free coming out. No other account in Canada does both.

Nearly 484,000 Canadians used the FHSA in its first year, with over half of them in the 25 to 34 age range. The median contribution was $8,000, the maximum. The Canadians who found this account ran straight to the limit. The ones who have not found it yet are still saving the hard way.

There is one detail that matters more than any other. The clock starts when you open the account, not when you contribute. Contribution room accumulates from the date the account is opened. A young Canadian who opens an FHSA today and contributes nothing has still started the clock. A year from now they have $16,000 in available room. The single most expensive mistake a first-time buyer can make is waiting to open this account until they feel ready to contribute.

For a couple where both partners qualify, the numbers double. Two FHSAs, fully maximised, produce $80,000 in tax-free savings before investment growth, and before either of them touches an RRSP or a TFSA.

Tool Two: The RRSP Home Buyers’ Plan — The Tool That Got a Quiet Upgrade

Most Canadians have heard of the Home Buyers’ Plan. Fewer know that the federal government quietly doubled the withdrawal limit in 2024, and it is worth a serious second look.

A first-time buyer can now withdraw up to $60,000 from their RRSP, tax free, to use toward the purchase of their first home. The withdrawal is not counted as income. No tax is withheld. The amount is repaid back into the RRSP over fifteen years, starting the second year after withdrawal.

For a couple where both partners qualify, that is $120,000 in RRSP savings accessible for a down payment without a single dollar of tax consequence at the time of withdrawal.

Two things worth knowing. First, the funds must have been sitting in the RRSP for at least 90 days before the withdrawal, so last-minute contributions do not qualify. Plan ahead. Second, the repayment schedule matters. Any year you do not make your minimum repayment, that amount gets added to your taxable income. It is a loan from your future self, and your future self will notice if you do not pay it back.

Used correctly, the RRSP Home Buyers’ Plan is not a compromise. It is a bridge.

Tool Three: The TFSA — The Most Misused Account in Canada

The Tax Free Savings Account is the most flexible registered account Canadians have and, for many young people, the most wasted one.

A TD survey from November 2025 found that four in ten Gen Z and Millennial Canadians are not investing the money in their TFSAs. They are parking cash in an account that was designed to compound tax free, earning interest that barely keeps pace with inflation, while the account’s real power sits completely unused.

The TFSA contribution limit is $7,000 per year in 2025 and 2026. For a Canadian who has been eligible since the account launched in 2009, total accumulated contribution room is now $109,000. That is not a savings account. That is an investment account with a tax-free wrapper, and it should be treated accordingly.

For a first-time buyer who has already maximised their FHSA, the TFSA becomes the next best place to build a down payment, invested, growing and completely tax free on withdrawal. Unlike the FHSA, there is no restriction on what the money can be used for, which means it doubles as an emergency fund and a down payment reserve at the same time.

The Order of Operations and What the Numbers Actually Look Like

This is the part most financial articles skip, because it requires doing the arithmetic out loud. Let’s do it.

A single first-time buyer who maximises their FHSA over five years accumulates $40,000 in tax-sheltered savings before investment growth. Add a fully funded RRSP Home Buyers’ Plan withdrawal of $60,000, and they have access to $100,000 in registered savings before they touch a single dollar of personal cash savings or ask their parents for anything.

A couple where both partners qualify? That number doubles. Two FHSAs at $40,000 each. Two RRSP Home Buyers’ Plan withdrawals at $60,000 each. One hundred and sixty, one hundred and eighty, two hundred thousand dollars in registered savings, depending on how long they have been building, before either set of parents writes a single cheque.

On a $700,000 home, that is not a down payment problem. That is a plan.

The order matters. FHSA first. Open it today, contribute as much as you can, and let the room accumulate. RRSP second. Build it deliberately with the Home Buyers’ Plan in mind and remember the 90-day rule. TFSA third. Stop parking cash and start investing, because the tax-free growth you are leaving on the table today is the down payment you will be short of in five years.

A Word About Mortgage Protection and the Insurance Worth Having

When you sign a mortgage in Canada, the bank will offer you mortgage life insurance at the closing table. It looks like protection. For many families, it is not the protection they think it is.

Bank-issued mortgage insurance is a group policy. The critical difference that most buyers never learn until it is too late is this: the underwriting happens at the time of a claim, not at the time of application. That means the bank reviews your health history after you have passed away, and they can decline the claim at exactly the moment your family needs it most. The coverage also decreases as your mortgage balance decreases, while the premium you pay stays the same throughout. And if you switch lenders or refinance, the policy does not travel with you.

A personally owned life insurance policy works differently on every count.

The underwriting happens now, while you are young and healthy and the premiums reflect that. The benefit is fixed for the life of the policy, not tied to a declining mortgage balance. The policy belongs to you, not to the bank, which means it is fully portable and the proceeds go directly to your family to use as they choose.

The line worth remembering is this. Bank mortgage insurance insures the bank. Life insurance insures your family.

For a young couple buying their first home, a conversation about personally owned life insurance before the keys change hands is one of the most useful financial conversations they can have. It is almost always less expensive than people expect, and almost always more valuable than what is offered at the closing table.

Coming Back to Maya and Her Parents

Maya’s parents want to help. That instinct is one of the most human things there is, and this article is not here to talk them out of it.

But the most useful thing they can do right now, before they move a dollar of their own retirement savings, is make sure Maya knows these three accounts exist, understands how they work, and is using them in the right order. Because the government has already allocated meaningful help for exactly this situation. The question is whether Maya is in a position to receive it.

If she has opened her FHSA, great. If she has not, today is the right day.

If her RRSP has been building with the Home Buyers’ Plan in mind, excellent. If she has been treating it as an afterthought, there is still time to change that.

If her TFSA is invested rather than parked, she is already ahead of four in ten of her peers.

And if, after all of that, there is still a gap and her parents still want to help close it, that conversation will be cleaner, smaller and less costly to their retirement than it would have been without a plan.

Helping your child is noble. Helping them help themselves first is better. And making sure that your own retirement security is not quietly funding a problem the government already had a solution for, that is the conversation worth having before anyone opens the banking app.

A Note from KB

If this article made you think of someone, a daughter doing the math on her phone, a son who has been renting longer than anyone expected, a young couple who keep saying they are saving but have not quite found their footing, please pass it along. It was written for them as much as for you.

And if you would like to talk through what a first home savings plan looks like for your family, or what the right kind of mortgage protection looks like before the keys change hands, I am easy to reach.

As always, I wish you health and happiness.

With gratitude, KB Henry

This article is provided as a general source of information only and should not be considered personal financial, tax or legal advice. Individual circumstances vary. Please consult with a qualified financial advisor, tax professional or legal advisor before implementing any strategy discussed.